Buying a home together is one of the biggest financial commitments an unmarried couple can make. A cohabitation agreement for buying a house in Canada helps turn the difficult questions into written rules before the mortgage, title, and moving boxes make everything more complicated.

The key issue is simple: the legal title, mortgage documents, and actual money trail do not always tell the whole story. One partner may contribute more to the down payment. The other may qualify for the mortgage. Both may pay for renovations. If the relationship ends, those details can become expensive to reconstruct.

This guide explains what Canadian couples should decide before closing, what a cohabitation agreement can cover, and why province-specific legal review matters.

What is a cohabitation agreement when buying a house?

A cohabitation agreement is a private contract between unmarried partners who live together or plan to live together. When it is used for a home purchase, it can set out how the couple wants to handle:

- The down payment and deposit

- Title ownership

- Mortgage payments

- Property tax, insurance, condo fees, utilities, and repairs

- Renovations and improvements

- What happens if one partner wants to sell

- What happens if the relationship ends

- What happens if one partner dies or can no longer pay

For a broader overview, see Prenuply's cohabitation agreement Canada guide. If you are comparing relationship stages, our guide to prenups vs cohabitation agreements in Canada explains when each document is usually used.

Why buying a home makes a cohabitation agreement more urgent

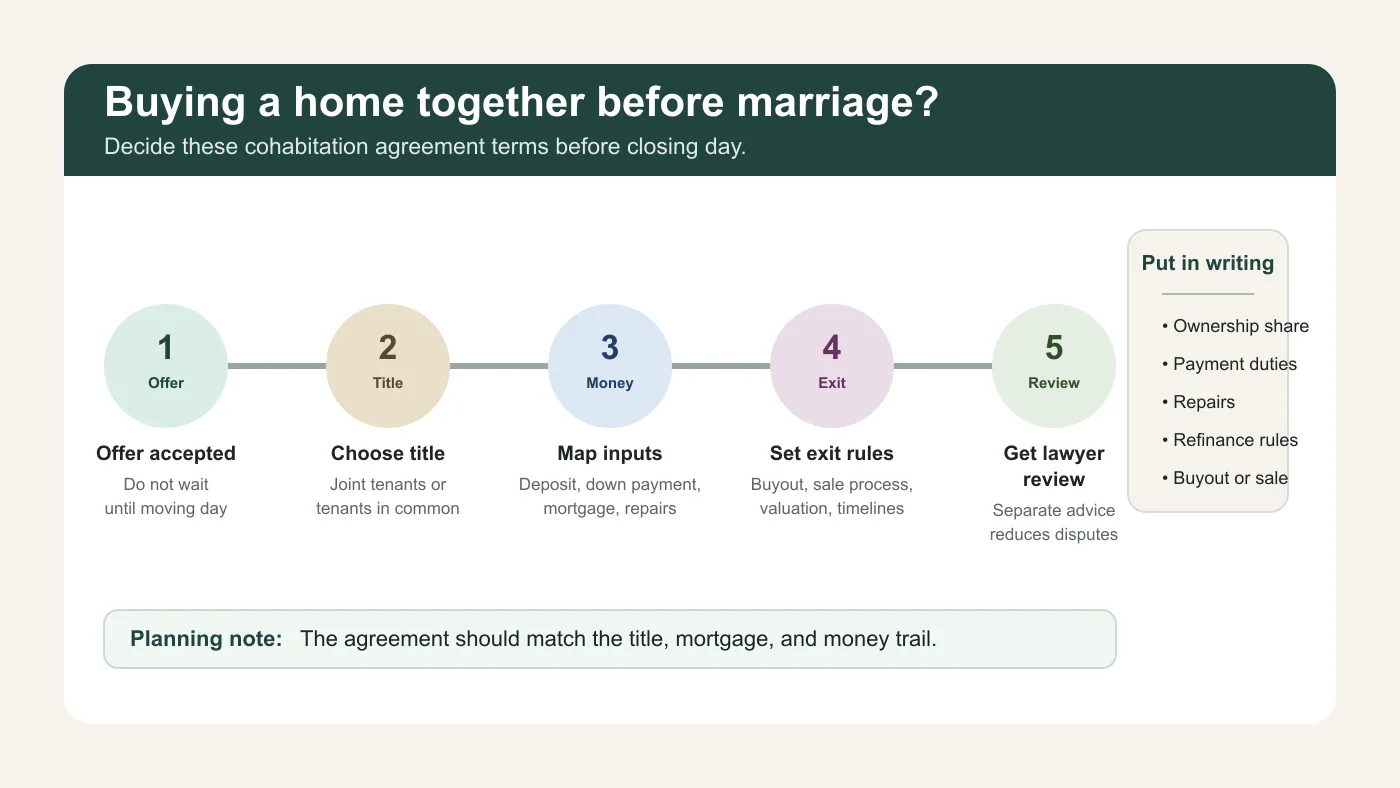

Before a home purchase, many cohabitation agreement questions are theoretical. After closing, the questions become attached to a mortgage, legal title, and hundreds of thousands of dollars.

The urgent issues usually fall into five buckets.

1. Title may not match contribution

A couple might choose joint tenancy because it feels equal, even if one partner paid most of the down payment. Another couple might choose tenants in common with unequal shares, but then split monthly costs equally.

Neither choice is automatically wrong. The problem is leaving the mismatch unexplained.

Ontario's co-ownership guidance encourages co-owners to use a legal contract to set out ownership, payment responsibilities, sale rules, and dispute resolution. That advice is not limited to romantic partners, but it is especially relevant when a couple is buying one home together.

2. The mortgage creates shared risk

If both partners sign the mortgage, each may be responsible to the lender even if the couple privately agreed to split costs another way. If only one partner signs the mortgage, the other partner may still be contributing money that should be documented.

A cohabitation agreement cannot rewrite the lender's mortgage contract. It can, however, record what the partners owe each other.

3. Repairs and renovations change the money picture

Down payment planning is only the start. A roof repair, basement renovation, new appliances, special assessment, or accessibility upgrade can create a second round of unequal contributions.

The agreement should say whether those payments are treated as ordinary shared expenses, added to one partner's contribution account, or handled another way.

4. Separation is harder when both people still own the home

If the relationship ends, one partner may want to keep the home and buy out the other. The other may want a quick sale. A written exit plan can reduce the chance that both partners are stuck paying a mortgage while arguing about price, timing, and listing decisions.

5. Common-law property rights vary by province

Canada does not have one simple common-law property rule. The default answer can change by province and by the length and nature of the relationship.

For example, Ontario public legal information explains that common-law partners do not have the same automatic property-sharing rules as married spouses. In British Columbia, family law rules can apply to people who have lived together in a marriage-like relationship for at least two years. Alberta has rules for adult interdependent partners. Manitoba also gives property rights to eligible common-law partners in specific circumstances.

That is why a generic template is risky for home buyers. The document needs province-specific legal review.

What should the agreement say about title?

Title is the legal ownership record for the property. It usually matters as much as the mortgage, sometimes more.

The two title structures couples often discuss are:

- Joint tenants: each owner has an undivided interest in the whole property, often with a right of survivorship.

- Tenants in common: each owner has a stated ownership share, which can be equal or unequal.

The right choice depends on the couple's province, estate plans, contribution split, lender requirements, and family situation. A cohabitation agreement should not treat title as a throwaway detail.

At minimum, the agreement should answer:

- Whose name will be on title?

- Will ownership be equal or based on percentage contributions?

- If one partner contributes more, is that a gift, a loan, or a reimbursable contribution?

- If title is joint but contributions are unequal, how will that be reconciled?

- If title is tenants in common, what percentage does each partner own?

- Does each partner's will and estate plan match the title choice?

This is one of the moments where legal advice matters. A lawyer can explain how title, survivorship, wills, tax, creditor risk, and family law interact in your province.

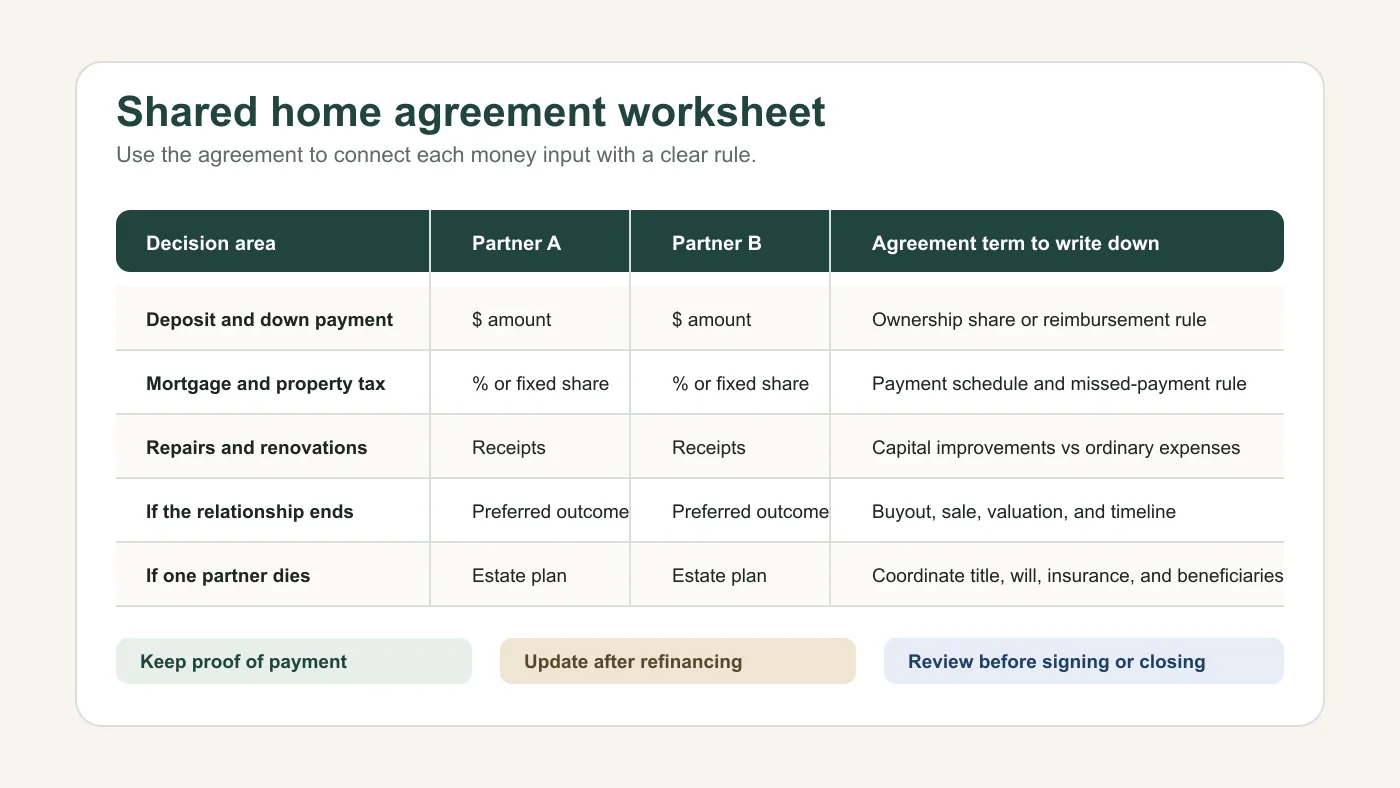

What should the agreement say about the down payment?

Down payment disputes are common because couples often focus on getting approved and closing on time. They do not always document what the money was meant to be.

Your agreement should identify each source of money:

- Partner A's savings

- Partner B's savings

- Gifts from either family

- Inheritance money

- Proceeds from a prior home

- RRSP Home Buyers' Plan withdrawals

- Borrowed funds

- Deposit paid with the offer

- Closing costs, land transfer tax, legal fees, and adjustments

Then decide how each contribution is treated.

For example:

- Equal ownership even if one partner contributes more

- Unequal ownership based on contribution percentages

- Equal ownership, but the larger down payment is reimbursed first on sale

- A family gift is excluded from sharing if the relationship ends

- A family loan must be repaid before equity is divided

If family money is involved, avoid vague wording. "My parents helped us" is not enough. Was it a gift to one partner, a gift to both partners, or a loan?

What should the agreement say about monthly costs?

Couples often say they will split everything 50/50, then discover their incomes, work schedules, or cash reserves do not make that realistic.

A better agreement explains the actual plan:

- Mortgage payment split

- Property tax split

- Home insurance split

- Condo fee or strata fee split

- Utilities

- Routine maintenance

- Emergency repairs

- Renovation budgets

- Furniture and appliances

- What happens if one partner loses income

If one partner pays more because they earn more, the agreement should say whether that larger payment changes ownership. If it does not, say so clearly. If it does, explain how.

What should happen if one partner wants out?

The exit plan is where a cohabitation agreement earns its value.

A practical exit plan can include:

- Who can trigger a sale or buyout

- Whether one partner gets a first option to buy the other's share

- How the home will be valued

- Which appraiser or valuation method will be used

- How long the buyout window lasts

- What happens if refinancing is not approved

- Who chooses the realtor if the home must be sold

- How sale proceeds are divided

- How mortgage penalties, realtor fees, legal fees, and repairs before sale are paid

Without these rules, a separating couple may have to negotiate while emotions are high and carrying costs continue.

How should renovations be handled?

Renovations can blur ownership quickly. A $7,000 appliance replacement might be a shared household cost. A $90,000 basement suite renovation may increase the property's value and create a much larger issue.

The agreement can separate:

- Ordinary repairs, such as plumbing fixes and appliance replacements

- Capital improvements, such as additions, major renovations, or structural work

- Cosmetic upgrades, such as paint and furniture

- Sweat equity, where one partner does unpaid labour

It can also require written approval above a dollar threshold. For example, the agreement might say that either partner can approve routine repairs up to a set amount, but major renovations require both partners to agree in writing.

Province-specific issues to discuss with a lawyer

The best cohabitation agreement for buying a house in Canada depends on the province where the property is located and where the couple lives.

Ontario

Ontario treats married spouses and common-law partners differently for many property issues. Ontario public information explains that married spouses generally have equalization rights, while common-law partners do not have the same automatic property division framework.

That makes written planning important for unmarried Ontario home buyers. See our dedicated Ontario cohabitation agreement guide for more detail.

British Columbia

In BC, spouses can include people who have lived together in a marriage-like relationship for at least two years. Family Law in BC explains that spouses can make agreements about property and debt while living together, and BC's property division rules may apply when qualifying spouses separate.

If you are buying in BC, review the title, down payment, excluded property, and family debt rules carefully. Prenuply's BC cohabitation agreement guide covers the province-specific starting points.

Alberta

Alberta has family property rules for adult interdependent partners. Alberta government guidance explains that unmarried partners can have property division rights under the Family Property Act if they meet the legal requirements.

If the home is in Alberta, ask a lawyer how adult interdependent partner status affects title, mortgage debt, and the agreement.

Quebec

Quebec uses a distinct civil-law framework. De facto spouses and married spouses can be treated very differently. If you are buying property in Quebec, speak with a Quebec notary or family lawyer before relying on a general Canadian agreement.

A simple worksheet for couples buying together

Use this as a planning checklist before you generate a draft or speak with a lawyer.

Gather:

- The accepted offer or purchase agreement

- Mortgage pre-approval or commitment letter

- Deposit receipt

- Down payment source details

- Gift letters or family loan documents

- Expected closing costs

- Draft title instructions, if available

- Monthly carrying cost estimate

- Renovation plans and budget

- Current wills and beneficiary designations

Then decide:

- Who owns what percentage

- Whether unequal contributions are gifts, loans, or reimbursable amounts

- Who pays each monthly cost

- What counts as a shared expense

- What counts as an ownership contribution

- Whether one partner can buy out the other

- How the home will be valued

- How long either partner has to refinance

- What happens if refinancing fails

- When the agreement should be reviewed or updated

Our cohabitation agreement checklist for Canada expands this into a broader relationship-planning checklist.

Should you sign before or after closing?

Usually, before closing is cleaner.

Signing before closing lets the agreement match the purchase structure from day one. It also gives each partner time to review disclosure, understand the title choice, and get independent legal advice before the money is committed.

After closing is still better than never, but it can be harder. The home is already owned, the mortgage is already signed, and one partner may feel pressure because changing the agreement could affect where they live.

If closing is coming up fast, do not rush a serious agreement the night before signing. A pressured agreement can create enforceability problems. Use the time you have to organize the facts, generate a working draft, and book legal review quickly.

Can Prenuply help create a first draft?

Prenuply helps Canadian couples create structured first drafts for cohabitation agreements and prenups. For home buyers, that means collecting the practical details a lawyer usually needs:

- Province

- Relationship status

- Property address details

- Title plan

- Down payment sources

- Mortgage and expense split

- Asset and debt disclosure

- Buyout or sale preferences

- Children or estate-planning considerations

- Special terms the couple wants reviewed

You can start a cohabitation agreement draft and use it as an organized starting point for legal review. Prenuply is not a law firm, and the draft should be reviewed by qualified lawyers before signing.

For cost planning, see our guide to cohabitation agreement cost in Canada.

FAQ: cohabitation agreement buying house Canada

Do unmarried couples need a cohabitation agreement to buy a house?

Not always, but it is strongly worth considering. Buying together creates title, mortgage, contribution, and exit-plan questions. A written agreement can reduce uncertainty if the relationship ends or one partner wants to sell.

Is a cohabitation agreement the same as a co-ownership agreement?

Not exactly. A co-ownership agreement usually focuses on property ownership between co-owners. A cohabitation agreement can include property ownership, but it can also address relationship-specific issues such as household expenses, support, debts, disclosure, and what happens if the partners later marry.

For couples buying together, the two concepts often overlap. A lawyer can decide whether one agreement is enough or whether separate documents make sense.

Can a cohabitation agreement say one partner gets their down payment back first?

Yes, it can usually be drafted to say that, but wording matters. The agreement should explain the amount, source of funds, whether the contribution is indexed or fixed, and what happens if the home sells for less than expected.

What if only one partner is on title?

That can create a major planning issue. The non-title partner may still pay mortgage costs, renovations, or household expenses. A cohabitation agreement can clarify whether those payments create reimbursement rights, ownership expectations, or no property claim between the partners.

What if we get married later?

Some cohabitation agreements continue after marriage. Others are replaced with a marriage contract or prenup-style agreement. If marriage is likely, ask your lawyer to draft with that transition in mind.

Do we each need our own lawyer?

Separate legal advice is strongly recommended. Independent advice helps each partner understand the agreement and can reduce later arguments about pressure, misunderstanding, or unfairness.

Bottom line

If you are buying a home together before marriage, do not leave the biggest questions until after closing. Decide how title, down payment, mortgage payments, repairs, renovations, buyout rights, and sale proceeds should work while both partners are still aligned.

A cohabitation agreement will not make every future issue easy. It can, however, give you a clearer starting point and a better record of what both partners intended.

Ready to organize the details? Create a cohabitation agreement draft with Prenuply, then have it reviewed by qualified lawyers in your province.

Sources used

- Ontario guide to co-owning a home

- Ontario information on dividing property when a relationship ends

- Family Law in BC on making an agreement when living together

- Family Law in BC on dividing property and debts after separation

- Alberta government information on dividing property between unmarried partners

- Manitoba information on common-law partners and property

This article provides general information about cohabitation agreements and shared home purchases in Canada. It is not legal advice. Prenuply AI Inc. is not a law firm and does not provide legal services. For advice about your specific situation, consult a qualified family lawyer in your province.