When one partner moves into a home the other partner already owns, the legal question is not just "who is on title?" It is also what the couple intended, who paid for what, whether the relationship later meets a provincial common-law threshold, and what should happen if the relationship ends.

A cohabitation agreement can turn that uncertainty into a written plan. It can confirm the homeowner's starting equity, explain whether the non-owner is paying rent or building a claim, set rules for renovations and mortgage contributions, and give both partners a fair exit process.

This guide is for Canadian couples where one partner owns the home before the other partner moves in. If you are buying a home together from the start, read our separate guide to a cohabitation agreement for buying a house in Canada.

Quick answer: do you need a cohabitation agreement if one partner owns the house?

Usually, yes. A cohabitation agreement is especially useful when one person owns the home and the other person will live there, pay household costs, help with renovations, or treat the home as the couple's shared residence.

Without an agreement, couples often rely on assumptions:

- The homeowner assumes title controls everything.

- The non-owner assumes regular payments create some protection.

- Both partners assume they will be fair later.

- Neither partner defines what "fair" means before money starts moving.

Those assumptions can be expensive. A written agreement can say whether the home remains separate property, whether mortgage or renovation contributions create reimbursement rights, how shared bills are handled, who can stay after separation, and what records each person should keep.

The agreement does not replace legal advice. It gives each partner and their lawyer a clearer draft to review.

Why a partner-owned home is different from a regular shared rental

A rental has a simpler baseline. The couple pays rent to a landlord, and neither partner is building equity in the property unless there is a separate ownership arrangement.

A partner-owned home is different because one partner may already have:

- equity built before the relationship,

- a mortgage in their name,

- property tax and insurance obligations,

- maintenance and repair risk,

- exposure to changes in market value,

- a strong emotional attachment to the home.

The non-owning partner may also be taking real risks. They may give up their own lease, move cities, contribute to mortgage payments, pay for improvements, take on more household work, or lose housing stability if the relationship ends.

A good agreement deals with both sides. It should not simply say "the owner keeps everything" without addressing the money and life changes the non-owner is making. It should also not treat every contribution as an ownership claim unless that is what both partners intend.

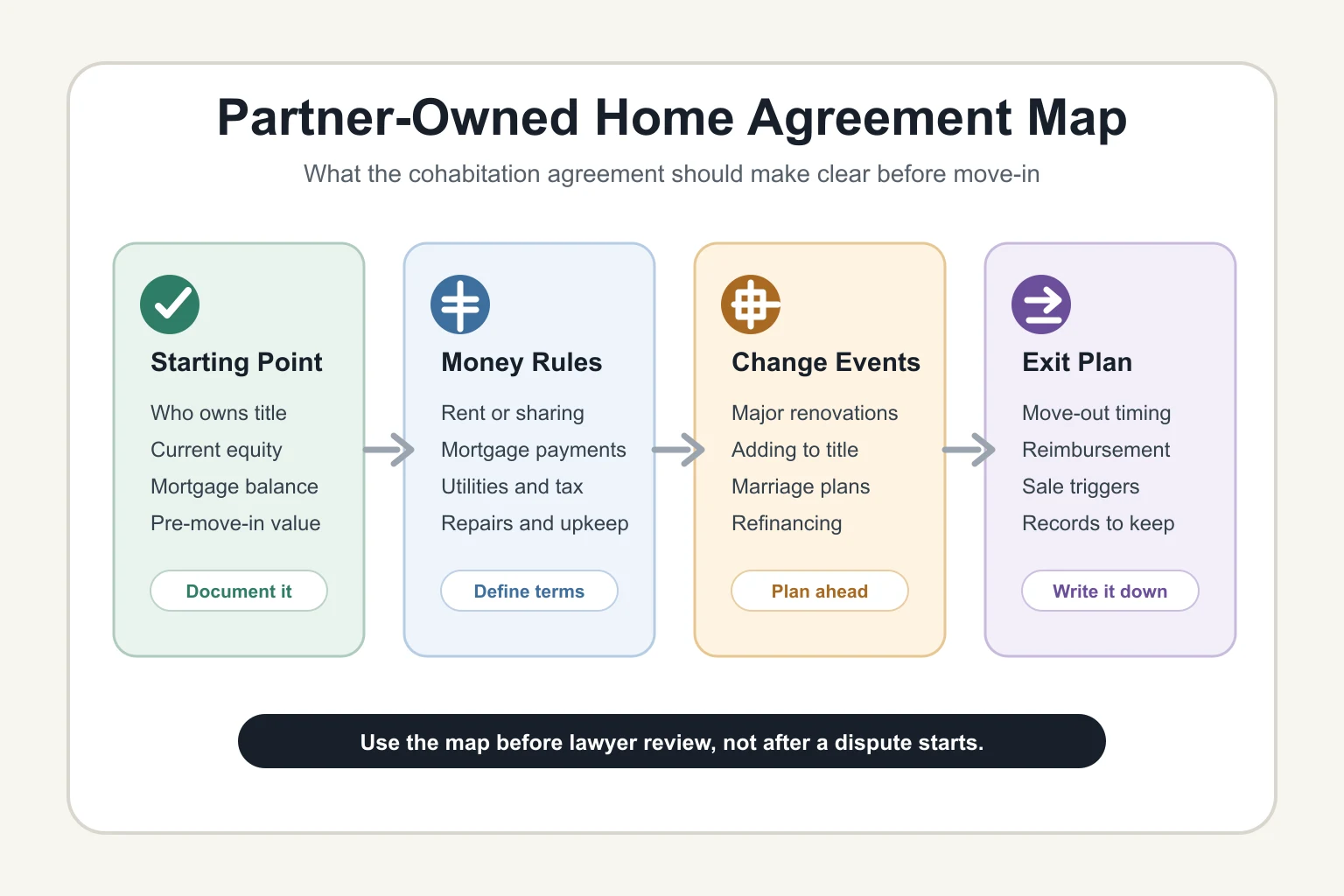

The planning map before move-in

Use this map before the move, before a major renovation, or before the non-owner starts paying more than ordinary shared expenses.

The core idea is simple: write down the starting point first, then decide how future contributions will be treated. That sequence matters because many disputes start when couples try to reconstruct old intentions after the relationship has already broken down.

What the agreement can say about the home

A cohabitation agreement can be practical and specific. It does not need to turn the relationship into a business transaction, but it should answer the questions that create disputes.

1. Who owns the home at the start

The agreement should identify the homeowner, the address, and the ownership status. It can also attach or reference supporting records, such as:

- title or deed information,

- mortgage balance,

- estimated property value at move-in,

- home equity line of credit balance,

- property tax and insurance obligations,

- any parent loans or family gifts connected to the home.

This starting snapshot is useful even if both partners are comfortable with the owner keeping the home. It gives everyone a shared baseline.

2. Whether payments are rent, shared expenses, or equity contributions

This is the most important section for many couples.

If the non-owner pays a monthly amount, what is it? It could be rent, a contribution to shared living costs, a contribution toward the mortgage interest only, a contribution toward principal, or a temporary arrangement while the couple saves for another goal.

Those choices can lead to different expectations. The agreement can say, for example:

- the non-owner's payment is a fixed household contribution and does not create ownership,

- mortgage principal remains the owner's responsibility,

- utilities, groceries, internet, and ordinary household costs are shared in a set percentage,

- extra payments toward principal require a written update,

- if the non-owner contributes to principal, the agreement defines whether that creates reimbursement, a percentage claim, or no claim.

The goal is not to pick one right answer. The goal is to avoid pretending the answer is obvious.

3. Repairs, maintenance, and renovations

A partner-owned home often creates a grey area between ordinary household costs and value-adding improvements.

The agreement can separate:

- routine expenses, such as lightbulbs, cleaning supplies, minor repairs, and small replacements,

- owner costs, such as major structural repairs, roof replacement, mortgage principal, property tax, and capital expenses,

- shared lifestyle improvements, such as paint, furniture, landscaping, or appliance upgrades,

- value-adding renovations, such as basement finishing, kitchen remodels, additions, or accessibility upgrades.

If the non-owner pays for a major renovation, the agreement should say whether that payment is a gift, a loan, a reimbursable contribution, or a contribution that changes the property-sharing arrangement. It should also say how receipts and proof of payment will be kept.

4. Appreciation in value

Some provinces may treat growth in value differently depending on the relationship status and the property rules that apply. Even where title matters a lot, a non-owner may still try to claim compensation if their money, labour, or sacrifices enriched the owner.

The agreement can address appreciation directly. For example, it can say:

- the owner keeps all pre-relationship equity,

- the owner keeps all appreciation unless the agreement is amended,

- the non-owner receives reimbursement for specific contributions only,

- the non-owner receives a defined percentage of value growth after a certain date,

- the couple will obtain a valuation if they separate.

If the home is the main asset in the relationship, this section deserves lawyer review. Small wording changes can have large consequences.

5. What happens if the relationship ends

The agreement should answer practical separation questions before anyone is upset:

- Who can stay in the home immediately after separation?

- How much notice does the non-owner receive before moving out?

- Are temporary expenses shared during the move-out period?

- What happens to furniture, pets, security deposits, and shared purchases?

- How will reimbursements be calculated and paid?

- Who pays for a valuation if one is needed?

- What happens if the owner wants to sell soon after separation?

This section protects the homeowner from a messy occupancy dispute. It also protects the non-owner from being left without a workable transition plan.

6. What happens if you later marry

If you plan to marry, ask a lawyer how your cohabitation agreement should interact with a marriage contract or prenup.

In Ontario, the Family Law Act says a cohabitation agreement is deemed to be a marriage contract if the parties later marry each other. Other provinces have their own contract rules and terminology. Either way, a couple that starts common-law and later gets engaged should not assume the original draft still fits the next stage of the relationship.

This is especially important for a home. Marriage can change family-home rights, possession rights, and property-division analysis in ways that may not apply while the couple is unmarried.

Province notes for a partner-owned home

Canadian family law is provincial. The same living arrangement can be treated differently depending on where the couple lives.

Ontario

Ontario common-law couples are not automatically required to split property acquired while they lived together in the same way married spouses divide net family property. That does not mean a partner-owned home is risk-free. A non-owner may still make equitable claims, such as unjust enrichment or constructive trust, if the facts support it.

Ontario also has a specific domestic-contract framework. A cohabitation agreement can deal with ownership or division of property, support obligations, and other settlement matters, subject to legal limits. It should be in writing, signed, and witnessed, and each partner should get independent legal advice.

For Ontario-specific context, see our Ontario common-law cohabitation agreement guide.

British Columbia

BC is different from Ontario. In BC, property-division rules apply to unmarried couples who have lived together in a marriage-like relationship for at least two years. The province explains that couples generally share property acquired during the relationship, while property brought into the relationship is treated differently. Couples can also make agreements if they do not want the default rules to apply.

For a partner-owned home, this makes the starting value and later value growth very important. If one partner owned the home before cohabitation, the couple should discuss how the agreement treats the original equity, mortgage reduction, renovations, and appreciation.

For more detail, read our BC cohabitation agreement guide.

Alberta

Alberta uses the concept of adult interdependent partners. Alberta's public guidance explains that adult interdependent partners can include people who live together in a relationship of interdependence for at least three years, have a child together in a relationship of some permanence, or enter into an adult interdependent partner agreement.

Alberta's Family Property Act property-division rules can apply to adult interdependent partners. Alberta also allows partners to opt out and draft their own agreement if they want to divide property differently, but lawyer advice matters.

For Alberta-specific context, read our adult interdependent partners guide.

Quebec

Quebec treats de facto unions differently from many other provinces. Quebec government guidance explains that, if you are not married or in a civil union, the Civil Code rules for family patrimony generally do not apply to you. It also notes that a cohabitation agreement can help de facto spouses decide how property should be divided if they separate.

Quebec has also introduced parental union rules for some couples with children. Because this is a technical area and notarial advice may be important, Quebec couples should speak with a Quebec notary or lawyer before relying on a draft.

Other provinces and territories

Rules vary across Canada. Some provinces give common-law partners property-sharing rights after a threshold is met. Others rely more heavily on title, equity claims, or specific statutes. The more money is tied up in the home, the more important local legal advice becomes.

Questions homeowners often want answered

Can my partner get half my house just by moving in?

Not automatically in every province, and not just because the relationship starts. But the better answer is province-specific. Time together, title, contributions, relationship status, children, marriage plans, and provincial property law all matter.

A cohabitation agreement can reduce uncertainty by saying what both partners intend before the non-owner moves in or starts contributing.

Should I charge my partner rent?

Maybe, but define it. If the payment is rent, the agreement should say that clearly and explain what it covers. If the payment is meant to replace shared rent that both partners would otherwise pay elsewhere, say that. If it is a mortgage contribution or a reimbursement arrangement, say that instead.

The label should match the reality. Calling a payment "rent" while both partners treat it as a home investment can create conflict later.

Can I keep all equity and still be fair?

Sometimes, yes. Many couples agree that the owner keeps pre-relationship equity and remains responsible for owner-level risks. Fairness may then come from lower monthly payments for the non-owner, reimbursement for major contributions, a reasonable move-out period, or a clear plan if the couple later buys a different home together.

Fair does not always mean 50-50. It means the arrangement is clear, informed, and realistic.

Questions non-owners often want answered

What if I help pay the mortgage?

Ask what part of the mortgage you are paying. Interest, principal, property tax, insurance, utilities, and repairs are not the same thing.

If your payment helps reduce principal, you may want the agreement to say whether you receive reimbursement or some other defined benefit if the relationship ends. If you are paying a set household amount instead, the agreement should say that it does not create ownership unless you both later amend the agreement.

What if I pay for renovations?

Do not rely on memory. For major improvements, the agreement should say whether your contribution is a gift, a loan, reimbursable, or part of a value-sharing formula. Keep receipts, before-and-after photos, transfer records, contractor invoices, and any written approval from the homeowner.

What if I give up my apartment to move in?

The agreement can include a transition plan. That might mean notice before move-out, temporary expense sharing, storage cost rules, or a reimbursement mechanism for specific costs if the relationship ends soon after move-in.

This does not need to be adversarial. It is basic housing stability planning.

What to prepare before lawyer review

Before you send a draft to lawyers, gather:

- the property address and title details,

- the mortgage balance at move-in,

- a recent property value estimate or appraisal if available,

- details of any home equity line of credit,

- monthly carrying costs,

- a list of expected household contributions,

- renovation plans and budgets,

- existing debts connected to the home,

- any parent loans, gifts, or informal family contributions,

- each partner's income, assets, and debts.

This overlaps with the general cohabitation agreement checklist for Canada, but a partner-owned home deserves extra attention because the home is often the largest asset.

What not to do

Avoid these shortcuts:

- Do not rely on a verbal promise about the house.

- Do not let one partner pay for major renovations without a written plan.

- Do not assume the same rule applies in every province.

- Do not hide debts, liens, family loans, or mortgage details.

- Do not sign right after a breakup threat or under pressure.

- Do not use a generic form that ignores the home, title, and contribution history.

- Do not forget spousal support, since property and support are separate issues.

For support planning, see our guide to spousal support in a prenup or cohabitation agreement in Canada.

Can you start with an online cohabitation agreement?

Yes, if the situation is suitable. An online draft can help couples organize the facts, choose the main terms, and create a first version for lawyer review. It is especially useful when the couple already agrees on the broad outcome but needs a structured way to capture the details.

A partner-owned home is not the place to skip legal review. The draft should be reviewed by independent lawyers, especially where the non-owner contributes to mortgage principal, major renovations, or business-linked financing.

If cost is the concern, read our cohabitation agreement cost guide. A clear draft can reduce back-and-forth, but it should not replace advice when a home is involved.

FAQ

Is this a cohabitation agreement or a prenup?

If you are unmarried and living together or planning to live together, it is usually a cohabitation agreement. If you are engaged or planning to marry, you may need a prenup or marriage contract, or a cohabitation agreement that is designed to continue after marriage depending on your province.

Read our guide to prenup vs cohabitation agreement in Canada if you are unsure which path fits.

Should the non-owner be added to title?

That is a major legal and financial decision. Adding someone to title can affect ownership, financing, tax planning, estate planning, creditor exposure, and breakup rights. Do not do it casually. If you want the non-owner to build an interest, your lawyer can help compare title change, reimbursement, loan, percentage-sharing, and future purchase options.

Does paying utilities create a claim to the house?

Utilities alone are usually easier to treat as shared living costs than ownership contributions, but context matters. Problems arise when utility payments are mixed with mortgage principal, renovations, unpaid labour, or sacrifices that increase the owner's wealth. The agreement should separate ordinary expenses from value-building contributions.

What if we already live together?

You can still make a cohabitation agreement after moving in. It may take more disclosure and more careful drafting because contributions may already have started. Gather records before lawyer review so the agreement can address what has already happened and what will happen going forward.

What if we later buy a new home together?

Your agreement should say whether it applies only to the current home or also to replacement property. If you later sell the owner-held home and use proceeds for a jointly occupied home, the agreement should explain how the original equity is traced and whether the new home is shared.

Sources checked

This article was prepared with reference to public legal information from Ontario's Family Law Act, Ontario's property division guidance, CLEO's common-law property division guide, the Government of British Columbia's common-law property page, Legal Aid BC's guide to living together agreements, Alberta's guidance on unmarried partner property division, and Quebec's de facto union guidance.

Bottom line

When one partner owns the house, a cohabitation agreement should do more than name the owner. It should document the starting equity, define monthly payments, handle renovations, explain what happens if you marry, and give both partners a practical exit plan.

That clarity protects the owner from unintended claims and protects the non-owner from making real contributions with no written understanding. The best time to write it down is before the move-in feels routine.