If your parents or another family member are helping with a home down payment, the legal question is bigger than "will the lender accept the funds?" Couples also need to decide what the gift means between them.

Is the money a gift to one partner only? A gift to both partners? A loan from parents? A contribution that should come back first if the home is sold? A prenup, marriage contract, or cohabitation agreement can help answer those questions before the money is mixed into a home.

This guide is for Canadian couples who are engaged, planning to marry, already buying a home together, or moving from common-law to marriage after family money has helped with a down payment. If you are buying before marriage, also read Prenuply's guide to a cohabitation agreement for buying a house in Canada. If one partner already owns the home, start with the guide to a cohabitation agreement when one partner owns the house.

Quick answer: can a prenup protect a down payment gift from parents?

Often, a prenup can help protect or clarify a parent-funded down payment, but the details matter. The agreement should identify who received the funds, whether they were a true gift or a loan, how the funds were used, whose name is on title, what happens to appreciation, and how the money should be handled if the relationship ends.

The agreement should also be consistent with the mortgage file. If the lender required a gift letter saying the funds are non-repayable, do not privately treat the same money as a hidden loan. If the parents expect repayment, the couple should speak with their mortgage broker, real estate lawyer, family lawyers, and tax or financial advisers before closing.

The safest planning starts before the funds move. Once money has passed through joint accounts, been used for closing, paid down a mortgage, or funded renovations, the facts become harder to reconstruct.

Why down payment gifts create family-law risk

A family gift feels simple in the moment. Parents want to help their child buy a home. The couple wants to qualify for a mortgage. Everyone is focused on the purchase deadline.

The risk appears later, usually when the relationship ends and the home has gained or lost value. The couple may disagree about what the family intended:

- One partner says, "My parents gave that money to me."

- The other partner says, "It helped us buy our home together."

- The parents say, "We expected that amount to come back if you separated."

- The mortgage file says, "The money was a non-repayable gift."

- The title may say one thing, while the couple's payment history says another.

A written agreement can reduce that gap. It can separate the mortgage approval question from the relationship planning question. It can also make the couple's disclosure package stronger, because both partners have a record of the money, documents, and assumptions before signing.

For a broader list of records to prepare, see Prenuply's financial disclosure checklist for prenups in Canada.

Gift letter, family gift, or parent loan: do not mix the labels

Down payment money often has two audiences: the mortgage lender and the couple.

For mortgage insurance, CMHC explains that traditional down payments can come from savings, a sale of property, or "a non-repayable financial gift from a relative." Lenders may also ask for proof of the source of funds and a gift letter. That gift letter usually tells the lender that the money does not have to be repaid.

That does not automatically decide every family-law issue between partners, but it is a document you should take seriously. If the lender file says the funds are a gift, while a private side agreement says the parents must be repaid, that inconsistency can create mortgage, fraud, contract, and family-law problems.

The better approach is to choose the structure honestly:

- If it is a true gift to one partner, document the donor's intention and the couple's agreement about how that gift is credited.

- If it is a true gift to both partners, document that everyone understands it will be shared.

- If it is a loan, disclose it properly and get advice before using it for mortgage qualification.

- If parents want security, ask lawyers whether a registered loan, promissory note, title interest, or other structure is appropriate and lender-approved.

A prenup or cohabitation agreement should not be used to hide debt from a lender. It should be used to make the couple's intentions clear.

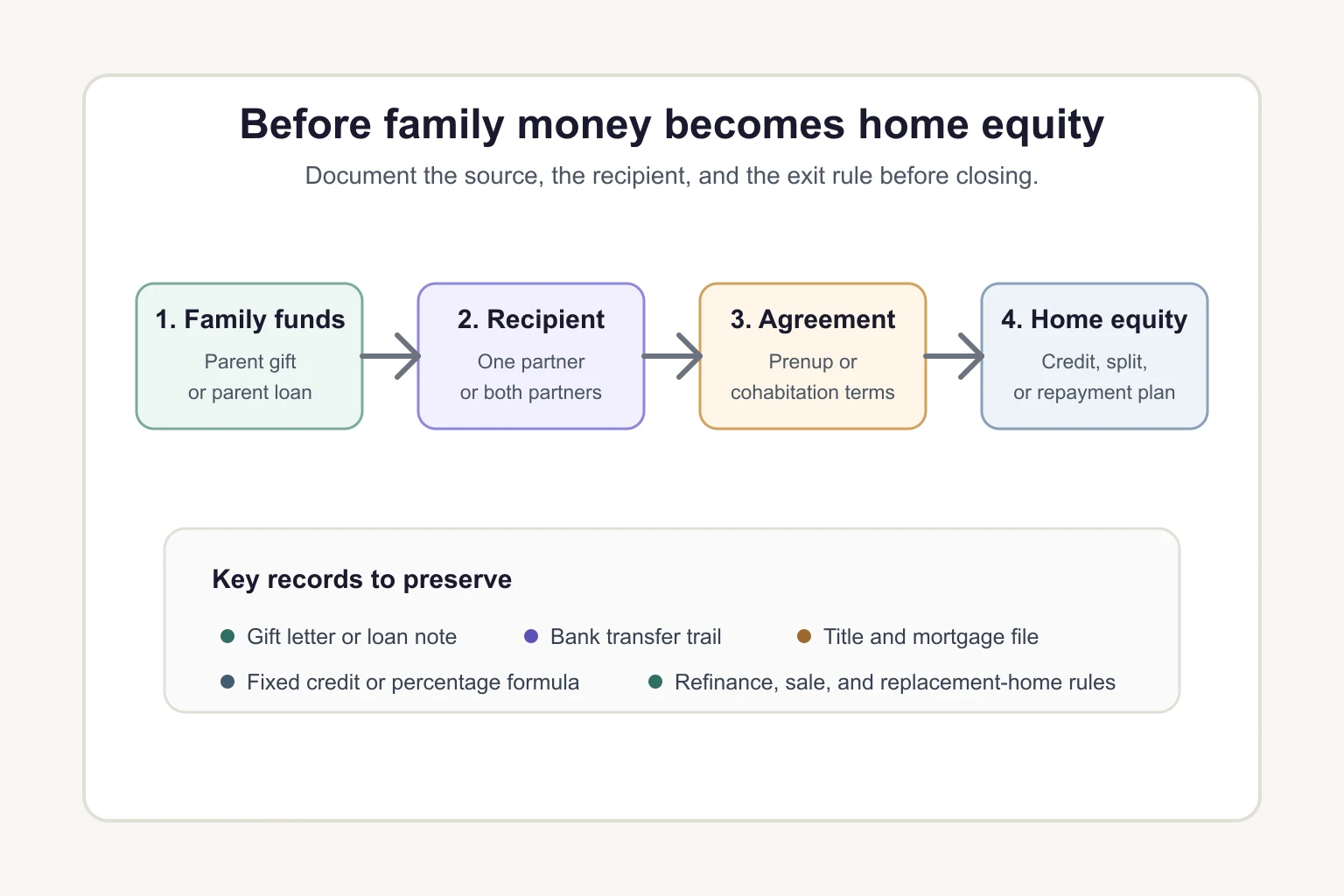

What the agreement should document before closing

The most useful prenup clauses start with a clean factual record. Before the gift is spent, collect:

- The donor's name and relationship to the recipient

- The amount, currency, and transfer date

- The account that received the funds

- Whether the gift was intended for one partner or both partners

- Whether any part is expected to be repaid

- Any gift letter, bank form, promissory note, or family letter

- The property address and purchase price

- The planned title ownership

- Each partner's own down payment contribution

- Closing costs, land transfer tax, legal fees, and mortgage details

- Whether the money will remain traceable in a separate account until closing

This information lets each partner and their lawyer understand what is being protected. It also helps avoid vague wording such as "family money will be returned first." That phrase can be too unclear unless the agreement says which family, what amount, from which source, and from what pool of money.

Four common ways couples handle parent-funded down payments

There is no single correct structure. The right fit depends on the province, mortgage, title, relationship stage, family expectations, and each partner's own contribution.

1. Gift to one partner with a first-credit clause

This is common when parents want to help their child, not the couple equally. The agreement can say the gift was made to one partner and that, if the home is sold after separation, that partner receives the first credit for the documented amount before remaining equity is divided.

The clause should also say whether the credit is fixed or adjusted. For example, a $100,000 gift could stay a fixed $100,000 credit, or it could receive a percentage share of appreciation. Those are very different outcomes.

2. Gift to one partner, but the home is shared equally after the gift is credited

Some couples want to protect the parent contribution while still sharing future growth. The agreement might say Partner A receives the first $100,000 of net sale proceeds because that came from Partner A's parents, then the remaining net equity is divided equally.

This can feel balanced when both partners will pay the mortgage and carry the home together after closing.

3. Gift to both partners

Sometimes parents truly intend to help the couple jointly. If so, the agreement can say the gift is shared and does not create a repayment, credit, or separate-property claim.

That clarity matters too. Without it, the recipient partner may later argue the gift was meant only for them, while the other partner believed it was family support for both.

4. Parent loan or secured contribution

If parents expect repayment, the structure needs more care. A real loan may affect mortgage qualification. It may need a promissory note, interest terms, maturity date, security, or disclosure to the lender. It may also affect the couple's net equity if they separate.

Do not solve this with a quiet handshake. If the money is a loan, get advice before signing any mortgage gift letter or closing documents.

What clauses can say in a prenup or cohabitation agreement

A strong down payment clause usually does more than name the gift. It should explain the mechanics.

Useful clauses can address:

- The source and amount of the parent contribution

- Whether the contribution is a gift or loan

- Whether the gift is to one partner or both

- Whether the recipient gets a fixed-dollar credit or percentage credit

- Whether appreciation on that credit is shared or separate

- Whether mortgage principal payments change the ownership split

- Whether renovations funded by either partner change the equity formula

- How sale proceeds are calculated after mortgage, sale costs, taxes, and debts

- What happens if the home is refinanced

- What happens if the couple buys a replacement home

- What records must be kept

- How the agreement changes if common-law partners later marry

If the couple is planning for marriage, the agreement should also fit with broader asset clauses. Parent gifts may interact with inheritance planning, future assets, debt, and support. For related planning, read Prenuply's guide to protecting inheritance with a prenuptial agreement in Canada and the guide to whether a prenup can protect future assets in Canada.

Province notes: why the same gift can be treated differently across Canada

Family law is provincial. A parent-funded down payment may raise different issues depending on where the couple lives and whether they are married, common-law, or adult interdependent partners.

Ontario

Ontario has special rules for the matrimonial home. The Family Law Act excludes some gifts and inheritances from net family property, but the statute carves out the matrimonial home. Ontario's public guidance also says that if the family home was gifted or inherited, it does not count as excluded property and must be divided equally unless the spouses agree to a different split.

That makes parent-funded home planning especially important for Ontario spouses. A gift that might look protected in another account may be harder to protect once it is used for a matrimonial home.

Ontario common-law couples are different. The province explains that common-law couples are not automatically required to split property acquired while living together, but claims can still arise where one partner contributed to property owned by the other. A cohabitation agreement can document the plan before contributions begin.

For more Ontario home context, read Prenuply's article on the Ontario prenup and the matrimonial home.

British Columbia

BC property division rules apply to married spouses and to unmarried couples who have lived together in a marriage-like relationship for at least two years. BC's public guidance explains that gifts and inheritances to one spouse can be excluded property, but the increase in value of excluded property during the relationship is family property.

That can matter where a parent gift becomes part of a home that appreciates. The original amount may be treated differently from the growth, unless the couple has an agreement that says something else and the agreement survives review.

Alberta

Alberta uses the term adult interdependent partners for many committed unmarried relationships. Alberta's public guidance says the Family Property Act applies to married spouses and adult interdependent partners, and that partners can opt out and draft their own property division agreement if they want to divide property differently.

For parent gifts, Alberta couples should document whether the money was intended for one partner or both, preserve records, and ask lawyers how exemptions, increases in value, title, and relationship timing apply.

Quebec

Quebec couples should be especially careful with terminology. Married spouses may need a marriage contract, often involving a notary. Unmarried de facto spouses generally do not have the same family patrimony framework as married or civil union spouses, but they can still use a cohabitation agreement to organize property, support expectations, and household finances.

If family money is being used for a Quebec home, speak with a Quebec notary or lawyer before relying on a generic Canadian clause.

Common mistakes to avoid

The biggest mistake is waiting until after closing. Other common mistakes include:

- Signing a mortgage gift letter while privately expecting repayment.

- Depositing parent funds into a joint account without records.

- Putting both partners on title without deciding whether ownership should match contributions.

- Assuming a gift from parents is automatically protected in every province.

- Forgetting that appreciation may be treated differently from the original gift.

- Treating renovations, mortgage principal, and carrying costs as if they are all the same.

- Using a fixed-dollar clause when the couple actually intends a percentage return.

- Forgetting what happens if the home is refinanced or replaced.

- Ignoring spousal support, which is separate from property division.

- Signing too close to the wedding or closing date, when pressure can become an issue.

For timing and pressure risks, see Prenuply's guide to whether a last-minute prenup in Canada is too late. For support planning, see the guide to spousal support in a prenup or cohabitation agreement in Canada.

A practical checklist before family money moves

Before parents send the funds, ask these questions:

- Who is the intended recipient, one partner or both?

- Is the money a true gift, a loan, or something else?

- Will the lender require a gift letter?

- Are the parents expecting repayment, security, or influence over title?

- Will both partners be on title?

- Will both partners pay the mortgage?

- Should the recipient receive a fixed credit or percentage credit?

- How will renovations and mortgage principal be treated?

- What happens if the couple separates before marriage?

- What happens if the couple marries after signing a cohabitation agreement?

- What records will each partner keep?

- When will each partner get independent legal advice?

If you can answer these questions calmly before closing, the agreement will be easier to draft and easier for lawyers to review.

Can Prenuply help?

Prenuply can help couples organize their information, identify the money and property terms they want to address, and create a Canadian prenup or cohabitation agreement template for lawyer review.

That can be useful when parent money is involved because the couple can start with a structured draft rather than a blank page. The draft should still be reviewed by independent lawyers, especially where a home, mortgage, parent loan, matrimonial home issue, or province-specific signing requirement is involved.

If you are ready to organize your agreement, you can create a Prenuply account and start building your draft.

FAQ

Is a parent down payment gift automatically protected in Canada?

No. Protection depends on the province, relationship status, title, timing, donor intention, records, agreement wording, and how the funds are used. A gift kept in a separate account may be easier to trace than a gift used for a shared home.

Should the gift go into a separate account?

Often, yes. Keeping funds in a separate account until closing can make the paper trail cleaner. If money is mixed with joint funds, spent on renovations, or used for general household expenses, tracing can become harder.

Can parents require us to sign a prenup?

Parents can set conditions for their own gift, but pressure matters. If one partner feels forced to sign an agreement to avoid losing the home purchase or wedding plans, that can create enforceability risk. Each partner should have time, disclosure, and independent legal advice.

What if the gift already happened?

You may still be able to make an agreement, but gather records first. Bank transfers, gift letters, mortgage documents, title records, emails, and closing statements can help lawyers understand what happened.

Is this a prenup or a cohabitation agreement?

If you are engaged or planning to marry, you may need a prenup or marriage contract. If you are unmarried and living together or buying before marriage, you may need a cohabitation agreement. If you later marry, ask a lawyer how the first agreement should carry forward.

Can an online prenup cover a parent gift?

An online tool can help organize the facts and create a starting draft. It should not replace legal advice when a home, mortgage, parent contribution, or province-specific property rule is involved. The stronger use case is to arrive at lawyer review with a clear, complete draft.

Sources checked

This article was prepared with reference to:

- CMHC mortgage loan insurance purchase guidance

- Ontario Family Law Act

- Ontario guidance on dividing property when a marriage or common-law relationship ends

- British Columbia guidance on family property and debt

- British Columbia Family Law Act

- Alberta guidance on dividing property between unmarried partners

Legal disclaimer

This article is general information for Canadian couples and is not legal, mortgage, tax, financial, or real estate advice. Laws, lending requirements, court approaches, and administrative processes can change, and the correct approach depends on your province, documents, mortgage file, title, relationship status, and facts. Prenuply AI Inc. is not a law firm and does not provide legal services.